.png)

Working Capital vs. Term Loan — Which One Does Your Business Actually Need?

Two of the most common business loans in India — and most borrowers don't know the difference until it's too late.

A business owner recently told us he had taken a term loan to manage his monthly vendor payments. He was paying EMIs on a five-year loan for expenses that cycled in and out every 30 days. He was, in his own words, 'paying for a highway when all I needed was a rickshaw lane.'

The wrong loan type costs you in two ways — financially, and in how it sits on your balance sheet. Getting this decision right is not complicated. It just requires understanding what each product is actually designed to do.

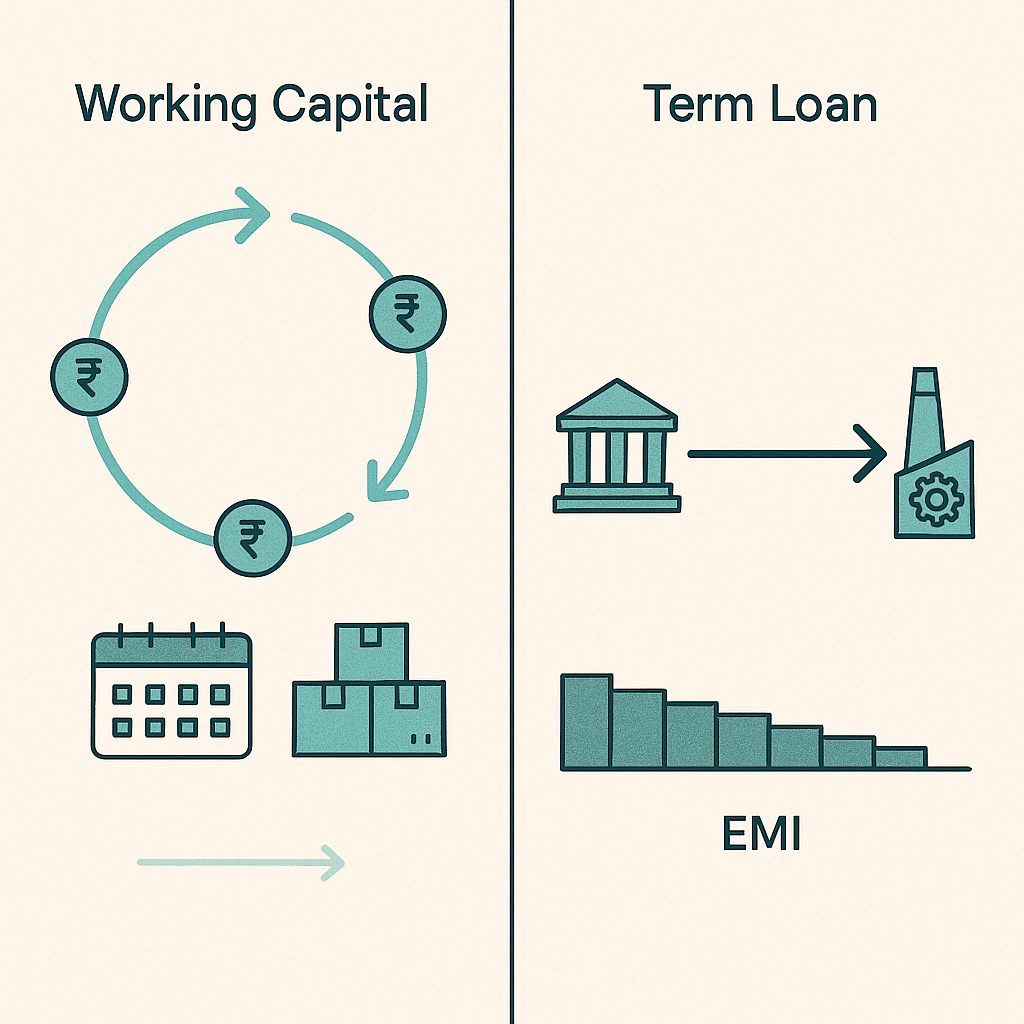

The simplest way to think about this

A term loan is like buying a house. You borrow once, for a fixed purpose, and repay in structured instalments over years. A working capital loan is like a rechargeable card — you draw when you need it, repay when cash comes in, and draw again next time. One is for building. One is for running.

| Working Capital Loan | Term Loan |

|---|---|

| For day-to-day operations | For a specific long-term asset or purpose |

| Revolving — repay and redraw | One-time disbursement, fixed repayment |

| Short tenure: 12–36 months | Long tenure: 3–10 years |

| Cash credit, OD, invoice discounting | Machinery, property, expansion |

| Sized to your revenue cycle | Sized to the asset or project cost |

| Interest on amount used | Interest on full disbursed amount |

How to decide which one you need — right now

Ask yourself one question: Is this expense recurring or one-time?

If the answer is recurring — salaries, inventory, vendor payments, operational costs — you need working capital. If the answer is one-time — a machine, a warehouse, a vehicle, an acquisition — you need a term loan. It is almost that simple.

Using a term loan for working capital is like using a fixed deposit to pay your grocery bill — structurally wrong. You end up with a long-term liability for a short-term need. The mismatch compounds over time and quietly damages your business's financial health.

Can you need both at the same time?

Absolutely — and many growing businesses do. A manufacturer might take a term loan to buy a new machine and simultaneously maintain a cash credit facility to fund raw material purchases. The key is that each product serves its purpose — and neither is asked to do the other's job.

Use working capital for what moves — inventory, expenses, cash cycles. Use term loans for what lasts — assets, infrastructure, expansion. Matching the loan to the need is half the battle.

Have a question about your finances?

FinAxis helps individuals and businesses across India with loans, working capital, wealth & insurance.

Talk to an expert