.png)

What Is CIBIL — and Who Is Actually Controlling Your Credit Score?

A three-digit number decides whether you get a loan, at what rate, and how fast. Here is who creates it and how it works.

CIBIL stands for Credit Information Bureau India Limited. It is India's oldest and most widely used credit bureau — a company that collects financial data on individuals and businesses, and compiles it into a credit report and credit score. When you apply for a loan, almost every lender in India pulls your CIBIL report within seconds as their first evaluation step.

Understanding who CIBIL is, where they get their data, and what they do with it is basic financial self-defence in modern India.

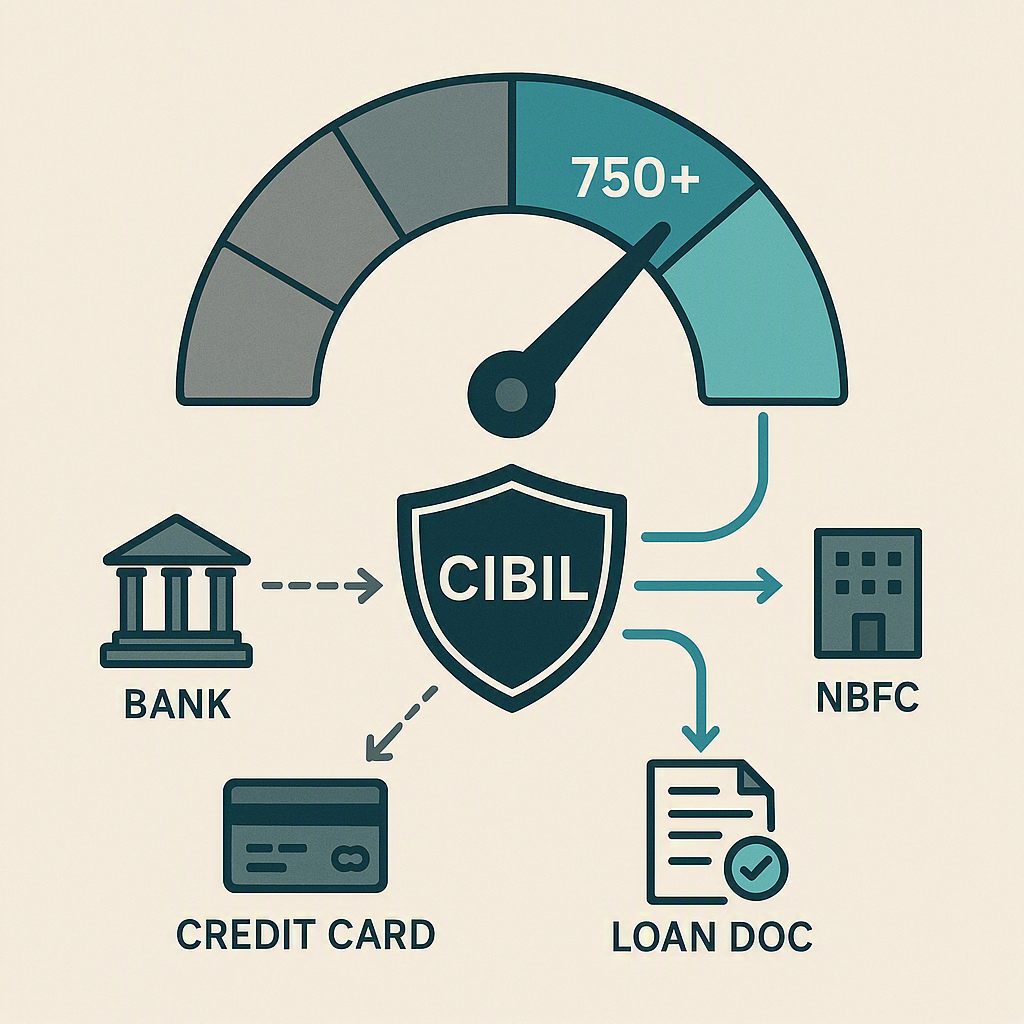

Where does CIBIL get its data?

CIBIL does not collect your data itself. It receives it — automatically and regularly — from every bank, NBFC, and credit card company you have ever borrowed from. Every time you miss a payment, repay an EMI, take a new loan, or close an account — your lender reports it to CIBIL within 30–45 days. This data is aggregated into your credit report, which forms the basis of your score.

You defaulted on a small credit card payment 4 years ago — a ₹3,000 balance you forgot to clear. The bank reported it to CIBIL. It is still on your credit report today, silently lowering your score. A loan officer reviewing your application 4 years later has no idea why you defaulted. They just see the red flag. This is why every payment — even small ones — matters permanently.

CIBIL is not the only credit bureau in India

While CIBIL is the most commonly referenced, India has four licensed credit bureaus: CIBIL, Equifax, Experian, and CRIF High Mark. Different lenders use different bureaus. Some use all four. Your report may differ slightly across bureaus depending on which lenders have reported to which bureau. It is worth checking your score across at least two bureaus.

| Credit Bureau | Key Coverage |

|---|---|

| CIBIL (TransUnion) | Most widely used by banks and large NBFCs |

| Equifax | Strong presence among credit card issuers |

| Experian | Growing presence — used by several fintech lenders |

| CRIF High Mark | Strong in MSME and microfinance lending |

How long does information stay on your report?

By RBI guidelines, negative information — defaults, late payments, settled accounts — stays on your credit report for 7 years from the date of reporting. Positive information — closed accounts, repaid loans — also remains, building your history. There is no way to delete accurate information from your report before this period expires. Time and good behaviour are the only remedies.

CIBIL is not your enemy. It is a mirror. It shows lenders exactly how you have treated credit in the past. Understand that every financial commitment you make — or break — is being recorded. Manage credit accordingly, always.

Have a question about your finances?

FinAxis helps individuals and businesses across India with loans, working capital, wealth & insurance.

Talk to an expert