.png)

Simple Interest vs. Compound Interest — The Difference That Decides Your Financial Future

Two types of interest. One makes banks rich. The other — if you understand it — makes you rich.

Interest is the price of money. When you borrow, you pay it. When you save or invest, you earn it. But not all interest works the same way. The difference between simple interest and compound interest is not a minor technicality. It is the central mechanic behind every loan you will ever take and every investment you will ever make.

Simple Interest — the straightforward one

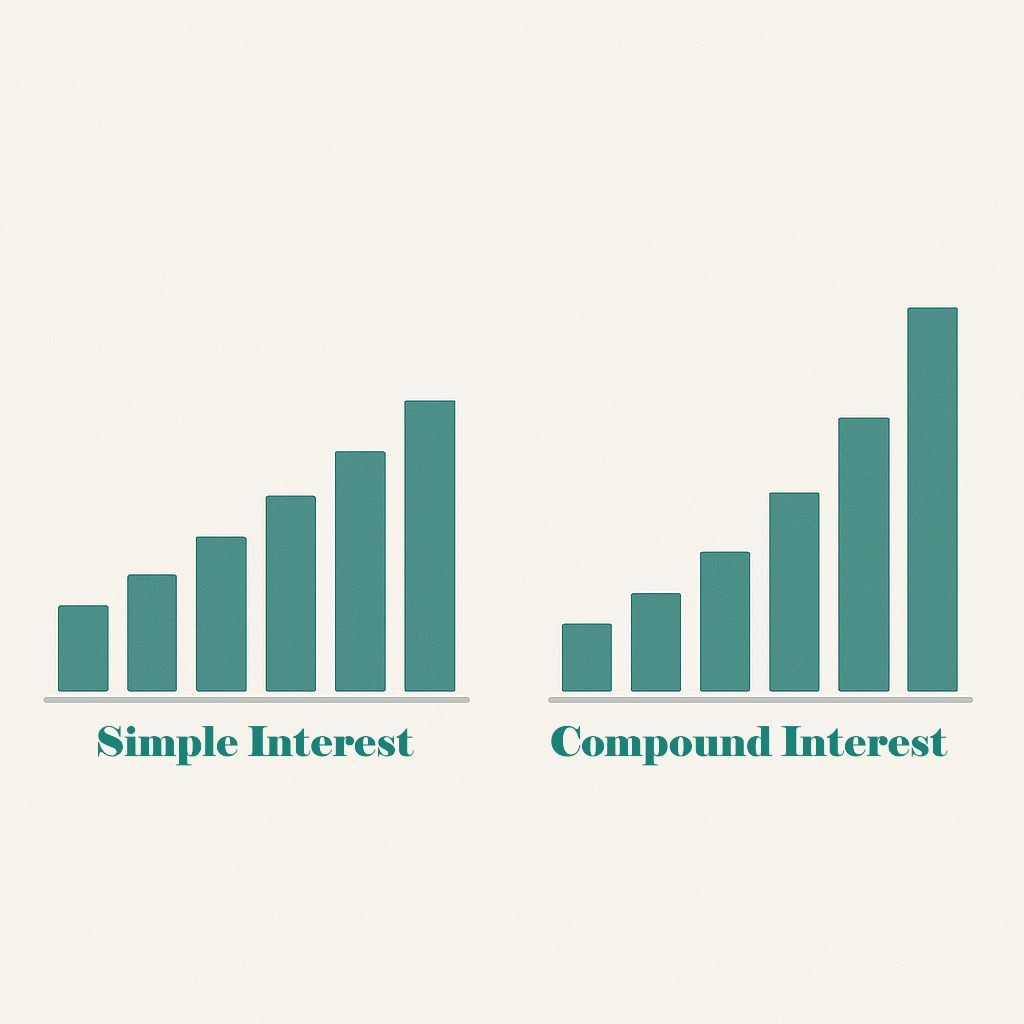

Simple interest is calculated only on the original principal. If you deposit ₹1 lakh at 10% simple interest per year, you earn ₹10,000 every year — on the original ₹1 lakh. After 10 years, you have ₹2 lakh. Clean, predictable, linear.

Most government bonds and some fixed deposits use simple interest. It is easy to calculate. But it does not grow on itself.

Compound Interest — where the magic happens

Compound interest is calculated on the principal plus all interest already earned. So in year two, you earn interest on ₹1.10 lakh — not just ₹1 lakh. In year three, on ₹1.21 lakh. The base keeps growing. The growth accelerates.

₹1 lakh at 10% simple interest for 20 years = ₹3 lakh. The same ₹1 lakh at 10% compound interest for 20 years = ₹6.73 lakh. Same rate. Same time. More than double the outcome — just because interest is compounding instead of staying flat. Now understand why every lender loves compound interest on loans — and why you should love it on investments.

| Simple Interest | Compound Interest |

|---|---|

| Interest on principal only | Interest on principal + previous interest |

| Grows linearly | Grows exponentially |

| ₹1L at 10% for 10 yrs = ₹2L | ₹1L at 10% for 10 yrs = ₹2.59L |

| Predictable, flat growth | Slow start, dramatic finish |

| Common in government bonds | Common in mutual funds, loans, FDs |

The compounding trap — how it works against you on loans

On most loans, interest compounds monthly. That means unpaid interest gets added to your principal — and next month, you owe interest on the higher amount. Credit card outstanding balances, for instance, compound at 36–42% per annum. Leave ₹50,000 unpaid for a year and you owe nearly ₹70,000. Two years — nearly ₹98,000. The math is unforgiving.

Compound interest is the most powerful force in personal finance. When it works for you — in investments — start early and never interrupt it. When it works against you — in loans — pay off debt fast, especially high-interest debt. The same mechanism either builds or destroys wealth. Which side you are on is your choice.

Have a question about your finances?

FinAxis helps individuals and businesses across India with loans, working capital, wealth & insurance.

Talk to an expert