.png)

Asset Allocation — Why What You Own Matters More Than What You Pick

The most proven insight in all of investing. Almost no one talks about it simply enough.

Most investing conversations focus on which stock to buy, which fund to choose, which sector is hot. Very little conversation happens about the decision that research consistently shows matters most: how do you divide your money across different asset classes?

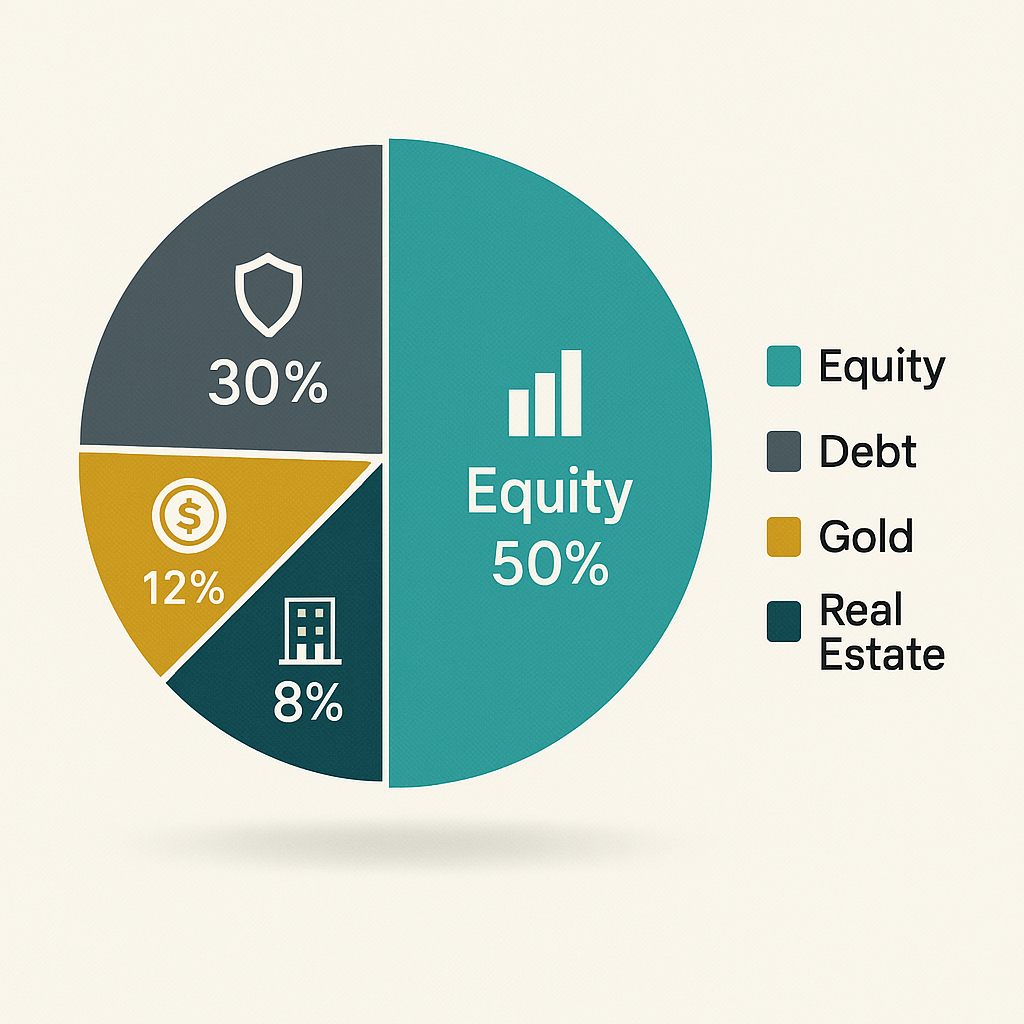

Asset allocation is the decision about what percentage of your wealth sits in equity, debt, gold, real estate, and cash. Studies suggest that 80–90% of a portfolio's long-term performance is explained by this allocation decision — not by which specific stocks or funds were chosen.

The four main asset classes — and what each does

| Asset Class | Role in a Portfolio |

|---|---|

| Equity (stocks/mutual funds) | Growth engine. Highest long-term returns. Highest short-term volatility. Best for goals 7+ years away. |

| Debt (bonds, FDs, debt funds) | Stability anchor. Predictable returns. Protects capital. Best for goals 1–5 years away. |

| Gold | Hedge against inflation and market crises. Tends to rise when equity falls. 5–10% allocation is common. |

| Real estate | Long-term store of value. Illiquid. Best for shelter or very long-term wealth, not short-term goals. |

How to decide your allocation

A simple starting framework is the 100-minus-age rule: subtract your age from 100 to get your equity percentage. A 30-year-old would hold 70% equity, 30% debt. A 55-year-old would hold 45% equity, 55% debt. This is not exact science — your risk tolerance, income stability, and specific goals refine it further.

During the March 2020 COVID crash, the Nifty 50 fell 38% in 5 weeks. An investor with 80% equity saw their portfolio drop significantly — and many panic-sold at the bottom. An investor with 50% equity and 50% debt saw a 19% drop — more manageable. They rebalanced, buying more equity at the lows. The second investor did not earn better returns because they picked better stocks. They earned better returns because their allocation allowed them to stay in the game.

Rebalancing — the discipline most investors skip

Over time, your allocation drifts. If equity performs well, it becomes a larger percentage of your portfolio than intended. Rebalancing means selling some equity and buying more debt to restore your target allocation — automatically forcing you to sell high and buy what is relatively cheap. Do this once a year. It takes one hour and has a measurable positive impact on long-term returns.

Pick your allocation before you pick your investments. Define how much goes in equity, how much in debt, and how much in gold — based on your timeline, your risk tolerance, and your goals. Then rebalance annually. This simple discipline outperforms most active stock-picking strategies.

Have a question about your finances?

FinAxis helps individuals and businesses across India with loans, working capital, wealth & insurance.

Talk to an expert